December 2022 Housing Market Trends Report

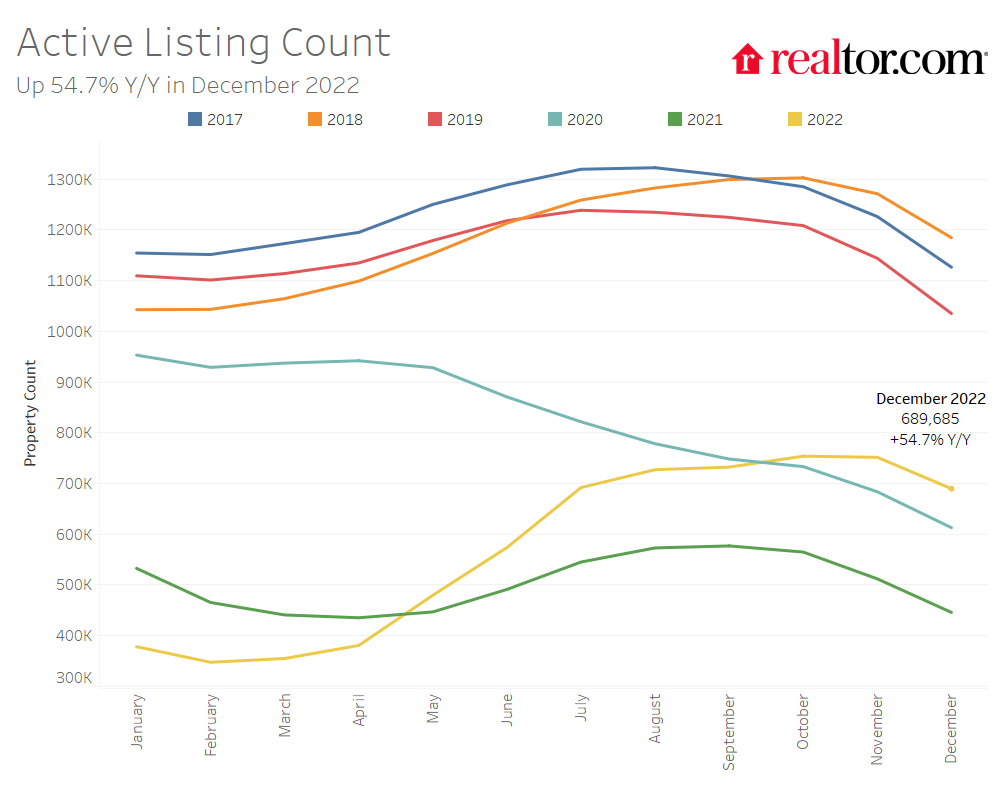

- The number of homes for sale has increased by 54.7% compared to last year.

- The total number of unsold homes, including homes that are under contract, has increased by 6.0% compared to last year.

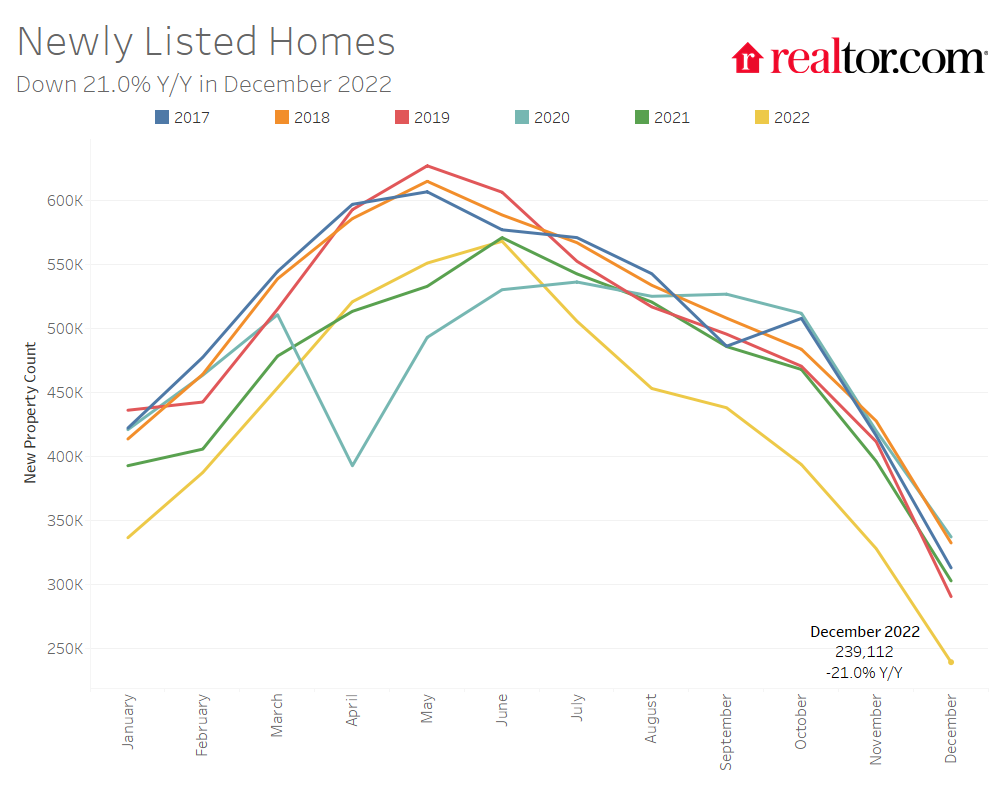

- Home sellers are less active this year, with 21.0% fewer homes being listed for sale compared to last year.

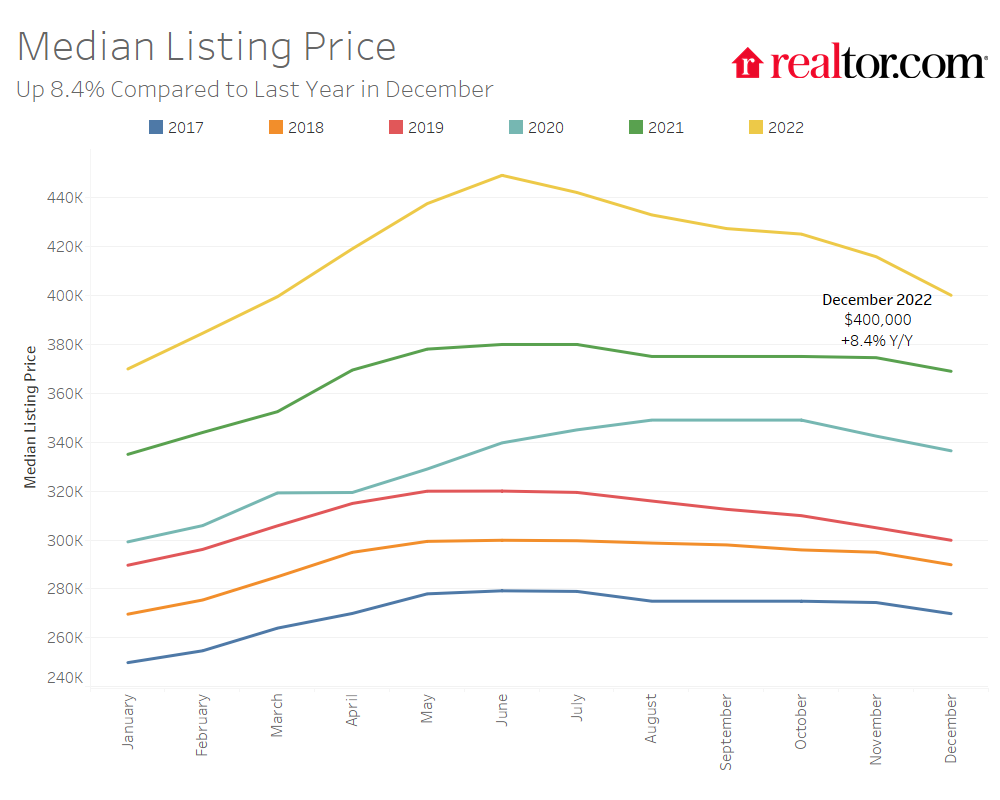

- The median price of homes for sale has increased by about 8.4% this month, but the rate of price growth has slowed down, entering single-digit territory for the first time in 12 months.

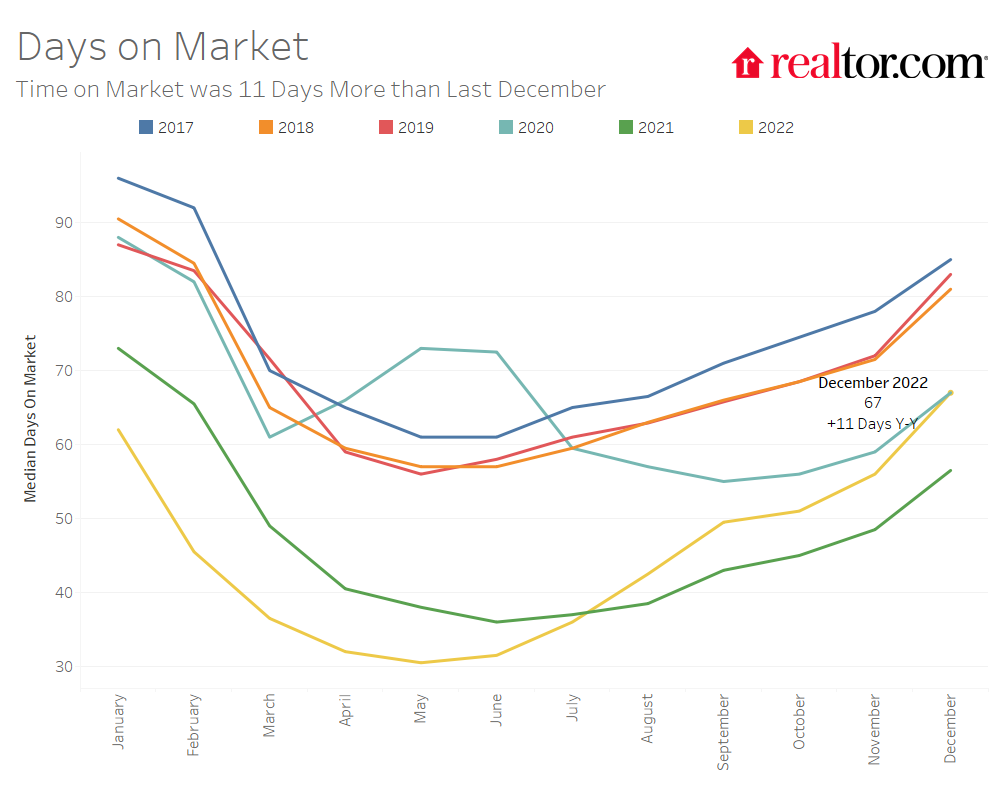

- Homes are spending 67 days on the market, which is eleven days longer than last year but still shorter than before the pandemic.

According to Realtor.com®’s December housing data, the housing market continued to cool, with inventory and time on market increasing and listing price growth dropping below 10% for the first time in a year. This gradually-cooling market offers some positives for homebuyers, as they may have more options and more time to make a decision on a home purchase. The year-over-year decline in pending home inventory increased only slightly compared to the previous month, possibly indicating that the market is starting to stabilize after pending listing declines worsened for the previous 11 months in a row. However, it’s important to keep in mind that the direction of inflation, mortgage rates, and overall economic growth will still impact the housing market in the coming months.

Housing Market Continues to See Increase in Inventory

There were 54.7% more homes for sale in December compared to the same time in 2021. This means that there were 244,000 more homes available to buy this past month compared to one year ago. While the number of homes for sale is increasing, it is still 38.2% lower than it was before the pandemic in 2017 to 2019. This means that there are still fewer homes available to buy on a typical day than there were a few years ago.

The total number of homes for sale, including homes that are under contract but not yet sold, increased by 6.0% compared to last year. Growth accelerated from last month’s 3.0% growth rate because homes are spending more time on the market, but the growth rate in the total number of homes for sale remains lower than active inventory because there are still fewer homes under contract (pending listings) than there were last year.

The number of homes under contract (pending listings) declined by 36.8% compared to the same time last year. This is very similar to November’s rate of decline, which could mean that the housing market is starting to stabilize at a relatively low level of existing home sales activity. However, this could change if the direction of inflation and mortgage rates changes in the months to come. Rising rates and home prices have increased the cost of financing 80% of the typical home by nearly $750 each month or 58.9% compared to a year ago, far outpacing recent rent growth (3.4%) and inflation (7.1%).

In December, the number of homes newly-listed for sale declined by 21.0% compared to the same time last year. This is a larger decline than last month’s 17.2% decrease. In November, home selling sentiment improved slightly compared to the previous month but remained well below last year’s levels. Fannie Mae’s Home Purchase Sentiment Index (HPSI) revealed that the net share of respondents saying now is a good time to sell increased by 6 percentage points compared to the previous month but declined by 20 percentage points compared to the prior year.

The number of homes for sale in the 50 largest cities in the U.S. has increased by 74.6% compared to last year. This is more than the national average. The West region has seen the most growth in the number of homes for sale, with a 110.2% increase compared to last year. The South region has seen the second-most growth, with a 103.9% increase. The Midwest and Northeast regions have seen slower growth, with 28.0% and 16.8% increases, respectively. Active listings in the West nearly reached pre-pandemic 2019 levels (-3.9%), while other regions are still well below this benchmark (-40.0% in the Midwest, -37.9% in the Northeast, and -26.7% in the South). In December, no regions saw new listing activity above the previous year. The South saw newly listed homes decline least, by 17.2% compared to the previous year, while they declined by 32.5% in the West, 21.8% in the Northeast, and 19.3% in the Midwest.

Inventory increased in 49 out of 50 of the largest metros compared to last year. Metros which saw the most inventory growth include Raleigh (+226.2%), Nashville (+226.0%), and Austin (+186.6). The only metro to see inventory decline on a year-over-year basis was Hartford (-7.7%).

In terms of newly-listed homes, only Nashville and Buffalo saw the number of newly listed homes increase in December compared to last year (+4.1% and 3.0%, respectively). Markets which reported large yearly declines in newly listed homes were all out West and included San Jose (-43.9%), San Francisco (-40.4%), Portland (-40.3%), and Seattle (-39.0%).

Home Are Spending More Time on the Market

The typical home spent 67 days on the market this December which is 11 days longer than the same time last year. Slower inventory turnover is primarily fueling the growth in actively listed homes but homes still spent 16 fewer days on the market this December than they did in the average December from 2017 to 2019.

In the 50 largest metropolitan areas in the United States, the typical home spent 61 days on the market, 11 days more than the previous December. This trend was seen across all regions, with larger metros in the West seeing the greatest increase (+18 days), followed by the South (+13 days), Northeast (+5 days) and Midwest (+5 days).

Out of the 50 largest metros, 45 saw an increase in time on market compared to the previous year. Of the 5 markets which saw shrinking time on market, the biggest declines were seen in Milwaukee (-16 days), and New Orleans (-5 days). Time on market increased most in Raleigh (+36 days), Phoenix (+34 days), and Las Vegas (+33 days).

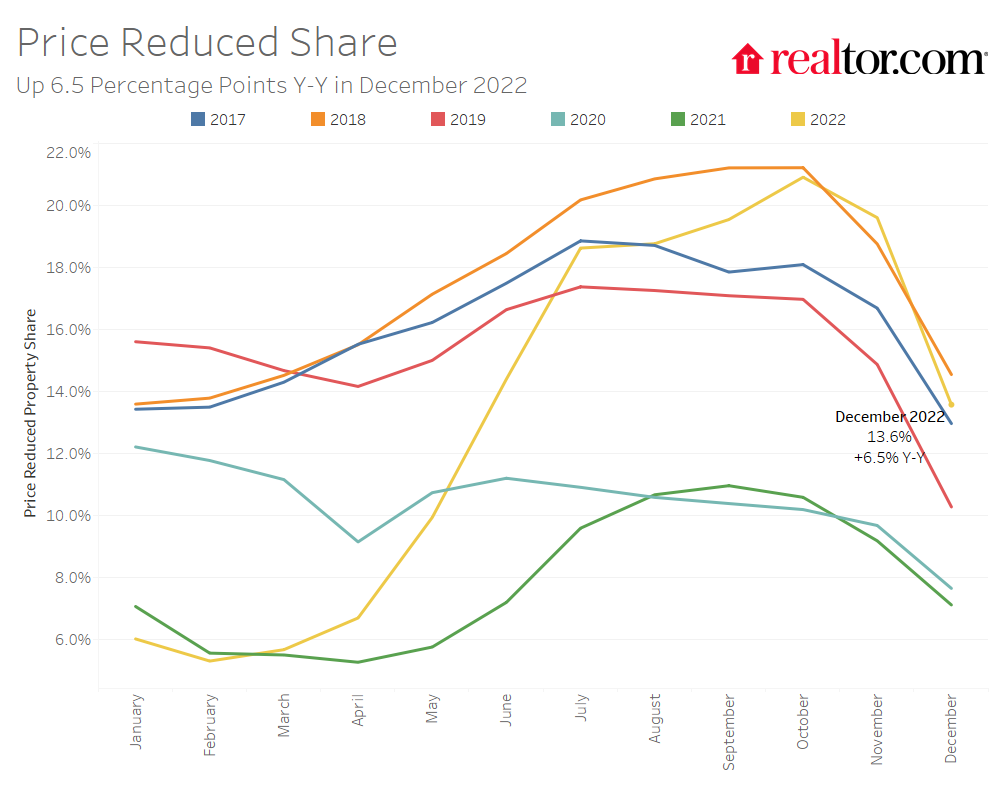

Price Growth Dips Below Double-Digits for First Time in 12 Months

The national median list price declined to $400,000 in December, down from a record high of $449,000 in June (-11.1%). This represents a yearly growth rate of 8.4%, which is lower than last month’s growth rate of 11.0%. This is the first time that listing price growth has fallen below double digits since December 2021.

The percentage of homes with price reductions increased from 7.1% in December of last year to 13.6% this year. This percentage is still higher than it was before the pandemic, but it is lower than the percentage seen in 2018 (14.5%).

In the largest metropolitan areas in the country, the combined annual median list price growth rate for active listings was 7.8%. Midwest metros had the highest growth rate in active listing prices, with an average increase of 12.2% over the past year. Prices in Milwaukee (+46.2%), Memphis (+34.0%), and Miami (+20.4%) saw the biggest increases among large metros. Southern metros saw the largest increase in the percentage of homes with price reductions (+9.6 percentage points), followed by Western metros (+8.7 percentage points). Phoenix (+17.3 percentage points), Austin (+15.5 percentage points) and Tampa (+15.3 percentage points) had the largest increases in the percentage of homes with price reductions compared to last year.

December 2022 Regional Statistics (50 Largest Metro Combined Average)

| Region | Active Listing Count YoY | New Listing Count YoY | Median Listing Price YoY | Median Listing Price Per SF YoY | Median Days on Market Y-Y (Days) | Price Reduced Share Y-Y (Percentage Points) |

| Midwest | 28.0% | -19.3% | 12.2% | 6.5% | 5 | 4.5% |

| Northeast | 16.8% | -21.8% | 8.1% | 3.9% | 5 | 2.6% |

| South | 103.9% | -17.2% | 8.0% | 5.7% | 13 | 9.6% |

| West | 110.2% | -32.5% | 3.0% | 1.1% | 18 | 8.7% |

December 2022 Housing Overview by Top 50 Largest Metros

| Metro | Median Listing Price | Median Listing Price YoY | Median Listing Price per Sq. Ft. YoY | Active Listing Count YoY | New Listing Count YoY | Median Days on Market | Median Days on Market Y-Y (Days) | Price Reduced Share | Price Reduced Share Y-Y (Percentage Points) |

| Atlanta-Sandy Springs-Roswell, Ga. | $399,900 | 2.6% | 3.2% | 62.2% | -20.5% | 60 | 12 | 16.2% | 9.6 pp |

| Austin-Round Rock, Texas | $525,000 | -3.4% | -1.2% | 186.6% | -18.8% | 73 | 27 | 24.6% | 15.5 pp |

| Baltimore-Columbia-Towson, Md. | $329,900 | 6.4% | 4.2% | 17.2% | -22.8% | 53 | 4 | 12.1% | 3.1 pp |

| Birmingham-Hoover, Ala. | $272,000 | -1.1% | 4.6% | 69.7% | -10.4% | 65 | 4 | 13.5% | 6.5 pp |

| Boston-Cambridge-Newton, Mass.-N.H. | $745,000 | 8.4% | -0.4% | 25.7% | -27.2% | 59 | 7 | 11.0% | 2.9 pp |

| Buffalo-Cheektowaga-Niagara Falls, N.Y. | $225,000 | 5.4% | 6.1% | 29.6% | 3.0% | 64 | -2 | 7.0% | 2.6 pp |

| Charlotte-Concord-Gastonia, N.C.-S.C. | $394,990 | 1.4% | 5.9% | 111.0% | -20.1% | 60 | 21 | 16.4% | 8.6 pp |

| Chicago-Naperville-Elgin, Ill.-Ind.-Wis. | $320,000 | 2.4% | -1.6% | 5.2% | -23.0% | 57 | 3 | 10.6% | 2.4 pp |

| Cincinnati, Ohio-Ky.-Ind. | $324,900 | 9.4% | 4.0% | 11.0% | -19.4% | 52 | 3 | 8.8% | 1.4 pp |

| Cleveland-Elyria, Ohio | $189,900 | 2.7% | 4.0% | 17.9% | -21.2% | 57 | 3 | 14.3% | 4.6 pp |

| Columbus, Ohio | $329,450 | 13.7% | 8.0% | 39.9% | -14.7% | 51 | 10 | 16.6% | 8.4 pp |

| Dallas-Fort Worth-Arlington, Texas | $435,213 | 8.8% | 5.7% | 160.8% | -9.1% | 59 | 17 | 18.7% | 13 pp |

| Denver-Aurora-Lakewood, Colo. | $600,000 | -4.0% | -4.7% | 146.2% | -29.6% | 61 | 21 | 17.8% | 12.2 pp |

| Detroit-Warren-Dearborn, Mich. | $229,900 | 6.0% | 2.2% | 39.4% | -12.5% | 56 | 11 | 17.4% | 4.5 pp |

| Hartford-West Hartford-East Hartford, Conn. | $359,000 | 4.8% | 1.4% | -7.7% | -29.8% | 65 | 10 | 7.3% | 2.1 pp |

| Houston-The Woodlands-Sugar Land, Texas | $359,900 | 0.0% | 2.0% | 49.8% | -5.3% | 60 | 6 | 14.0% | 4.8 pp |

| Indianapolis-Carmel-Anderson, Ind. | $290,000 | 5.5% | 7.6% | 77.8% | -17.8% | 55 | 9 | 18.1% | 9.6 pp |

| Jacksonville, Fla. | $386,990 | 5.3% | 6.0% | 144.7% | -12.7% | 67 | 17 | 20.4% | 14.6 pp |

| Kansas City, Mo.-Kan. | $409,900 | 19.7% | 10.0% | 61.4% | -29.0% | 77 | 19 | 10.6% | 4.7 pp |

| Las Vegas-Henderson-Paradise, Nev. | $440,000 | -2.2% | 4.2% | 108.0% | -23.4% | 74 | 33 | 19.5% | 9.4 pp |

| Los Angeles-Long Beach-Anaheim, Calif. | $891,000 | -1.8% | -1.6% | 92.1% | -31.4% | 70 | 21 | 10.2% | 5.8 pp |

| Louisville/Jefferson County, Ky.-Ind. | $290,000 | 13.3% | 4.5% | 33.4% | -33.3% | 51 | 10 | 16.7% | 5.8 pp |

| Memphis, Tenn.-Miss.-Ark. | $325,000 | 34.0% | 18.1% | 115.6% | -30.8% | 61 | 16 | 17.9% | 11.7 pp |

| Miami-Fort Lauderdale-West Palm Beach, Fla. | $590,000 | 20.4% | 9.2% | 52.7% | -14.8% | 68 | 5 | 13.5% | 8.1 pp |

| Milwaukee-Waukesha-West Allis, Wis. | $375,000 | 46.2% | 21.4% | 7.1% | -12.7% | 50 | -16 | 11.1% | 2 pp |

| Minneapolis-St. Paul-Bloomington, Minn.-Wis. | $400,000 | 11.9% | 6.6% | 9.8% | -16.1% | 58 | 7 | 10.8% | 4.2 pp |

| Nashville-Davidson–Murfreesboro–Franklin, Tenn. | $515,000 | 12.0% | 6.6% | 226.0% | 4.1% | 50 | 22 | 17.2% | 10.3 pp |

| New Orleans-Metairie, La. | $325,000 | -4.4% | -2.8% | 97.1% | -14.9% | 75 | -5 | 11.7% | 4.1 pp |

| New York-Newark-Jersey City, N.Y.-N.J.-Pa. | $658,944 | 6.5% | 5.6% | 4.0% | -29.1% | 81 | 5 | 6.7% | 1.7 pp |

| Oklahoma City, Okla. | $324,023 | 11.7% | 8.1% | 76.5% | -24.1% | 62 | 15 | 18.9% | 11.4 pp |

| Orlando-Kissimmee-Sanford, Fla. | $429,990 | 10.3% | 11.3% | 119.4% | -24.8% | 70 | 10 | 17.7% | 12.4 pp |

| Philadelphia-Camden-Wilmington, Pa.-N.J.-Del.-Md. | $320,000 | 6.7% | 4.1% | 15.7% | -23.1% | 66 | 8 | 11.7% | 3.3 pp |

| Phoenix-Mesa-Scottsdale, Ariz. | $474,500 | -2.4% | 2.7% | 165.5% | -21.3% | 70 | 34 | 25.5% | 17.3 pp |

| Pittsburgh, Pa. | $205,000 | -2.3% | -2.0% | 20.6% | -14.1% | 73 | 8 | 11.9% | 1.9 pp |

| Portland-Vancouver-Hillsboro, Ore.-Wash. | $589,000 | 7.3% | 2.3% | 91.5% | -40.3% | 66 | 16 | 12.8% | -1.9 pp |

| Providence-Warwick, R.I.-Mass. | $469,900 | 10.6% | 6.3% | 18.1% | -25.4% | 46.5 | -3 | 9.4% | 4.3 pp |

| Raleigh, N.C. | $446,000 | 5.7% | 3.4% | 226.2% | -17.0% | 71 | 36 | 17.0% | 11.7 pp |

| Richmond, Va. | $375,000 | 6.3% | 7.1% | 49.6% | -20.7% | 56 | 2 | 11.9% | 8.3 pp |

| Riverside-San Bernardino-Ontario, Calif. | $558,000 | 1.6% | 6.6% | 114.3% | -26.8% | 69 | 24 | 14.2% | 8.2 pp |

| Rochester, N.Y. | $237,000 | 20.3% | 16.0% | 16.8% | -23.6% | 44 | 5 | 8.9% | 2.1 pp |

| Sacramento–Roseville–Arden-Arcade, Calif. | $585,000 | -2.0% | -2.6% | 84.5% | -27.1% | 64 | 21 | 14.6% | 8.3 pp |

| San Antonio-New Braunfels, Texas | $349,000 | 3.5% | 2.9% | 99.3% | -18.0% | 68 | 19 | 18.6% | 10.7 pp |

| San Diego-Carlsbad, Calif. | $899,000 | 9.6% | 5.0% | 96.1% | -34.6% | 56 | 10 | 12.9% | 8.3 pp |

| San Francisco-Oakland-Hayward, Calif. | $990,000 | 4.6% | -2.6% | 57.1% | -40.4% | 63 | 15 | 9.8% | 6.1 pp |

| San Jose-Sunnyvale-Santa Clara, Calif. | $1,395,000 | 12.6% | -0.2% | 80.3% | -43.9% | 53 | N/A | 12.6% | 10.4 pp |

| Seattle-Tacoma-Bellevue, Wash. | $724,950 | 9.4% | 3.0% | 176.3% | -39.0% | 60 | 21 | 15.1% | 11.6 pp |

| St. Louis, Mo.-Ill. | $265,228 | 10.5% | 5.7% | 22.7% | -22.6% | 56 | 1 | 12.0% | 4.2 pp |

| Tampa-St. Petersburg-Clearwater, Fla. | $405,000 | 7.3% | 7.2% | 170.9% | -14.1% | 59 | 5 | 22.4% | 15.3 pp |

| Virginia Beach-Norfolk-Newport News, Va.-N.C. | $359,900 | 19.2% | 8.0% | 9.1% | -15.6% | 50 | 12 | 14.1% | 6.1 pp |

| Washington-Arlington-Alexandria, DC-Va.-Md.-W. Va. | $555,000 | 11.0% | -2.0% | 27.0% | -28.1% | 57 | 9 | 10.8% | 3.4 pp |

![]()

![]() Sabrina Speianu,

Sabrina Speianu, ![]()

![]() Danielle Hale,

Danielle Hale, ![]()

![]() Hannah Jones

Hannah Jones